What is the Interchange?

The interchange is the wholesale price charged to merchants for the authorization and settlement of credit card transactions.

Who set the Interchange fees?

The interchange fees are set by the credit card associations and are by far the largest component of the various fees that banks deduct from merchants’ credit card sales, representing 80% to 90% of these fees.

The interchange dictates the cost for all processing companies in the US and the interchange costs are exactly the same for all processors.

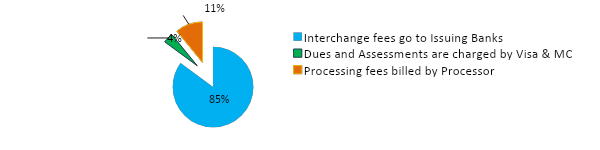

Who gets what?

Example of a retail merchant (card present, swiped cards):

Example of a $100 transaction:

Let’s assume a retail merchant’s global rate is 2.75% (Total fees divided by Total V/MC sales amount)

In this example, the total dollar amount of the fees would be $2.75.

- About 85% of these fees go to the issuing bank (so 2.34% or $2.34)

- The remaining 15% ($0.41) is split up between Visa or MasterCard, the processor and the sales office.

American Express Co., Discover Financial Services, LLC, Diners Club, Inc. and JCB International Credit Card. Co., Ltd. are not part of interchange, instead they set their own “wholesale costs”.

Also read: Mastercard is implementing new rules for merchants using subscriptions and recurring billing

Who sets the rates?

Visa and MasterCard establish the rates and qualification requirements for the each of the Interchange categories. Interchange is typically updated twice per year- in the spring and the fall. There are hundreds of different interchange categories. The rates can be found on the Visa U.S.A. and MasterCard Worldwide websites

Factors that affect merchant’s costs

Interchange fees have a complex pricing structure based on:

- The card brand (Visa and MasterCard have different rates)

- The type of card (credit or debit, rewards based, corporate, international etc)

- The merchant’s industry type (retailers, restaurants, wholesalers, Supermarkets, E-commerce, Schools, Gas stations etc..)

- The average ticket (smaller tickets get preferred item fees)

- How the merchant processes the transaction (swiped, keyed in, online, mobile).

Transactions are downgraded (to a higher cost category) when they don’t meet interchange requirements, including when the incorrect card information is captured at the POS, the transactions are settled late, or the transactions are key-entered rather than swiped, etc.

To further complicate the pricing structure, interchange fees are typically a percentage % of the total purchase price plus a flat fee.

Also read: How can merchants save money on their B2B credit card acceptance costs.

How to avoid extra costs?

An inaccurate account set-up can generate extra costs:

With Navidor’s expertise, merchants are confident they are qualifying for the best possible Interchange costs.

Learn more about Navidor Services